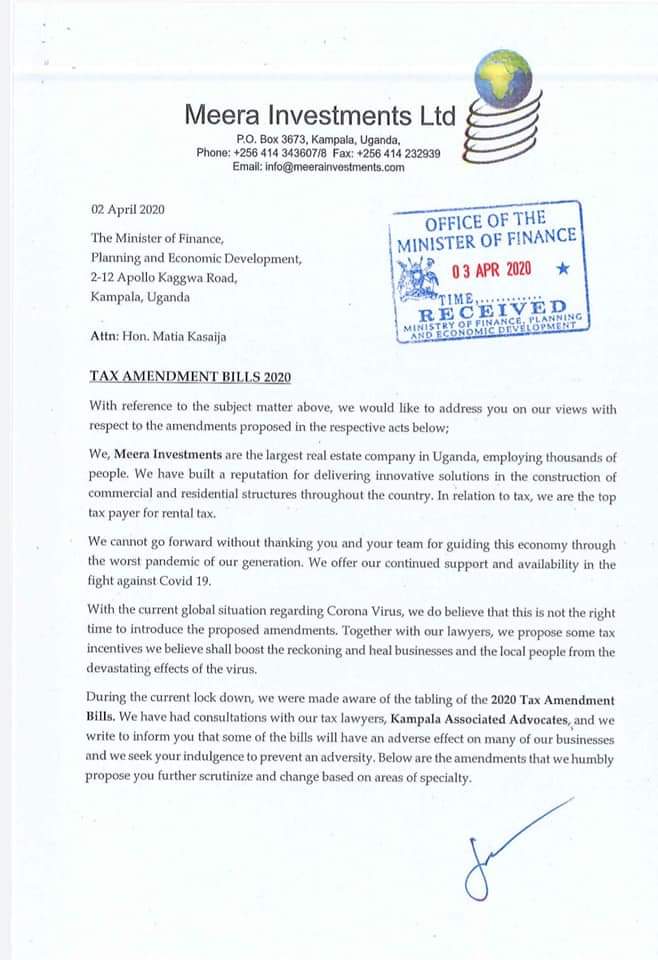

“During the current lockdown, we were made aware of the tabling of the 2020 Tax Amendments Bill. We have had consultations with our tax lawyer, Kampala Associated Advocates, and we write to inform you that some of the bills will have an adverse effect on many of our businesses and we seek your indulgence to prevent adversity,” the petition dated April 2 reads in part.

Part Of Meera Investments Petition reads in part

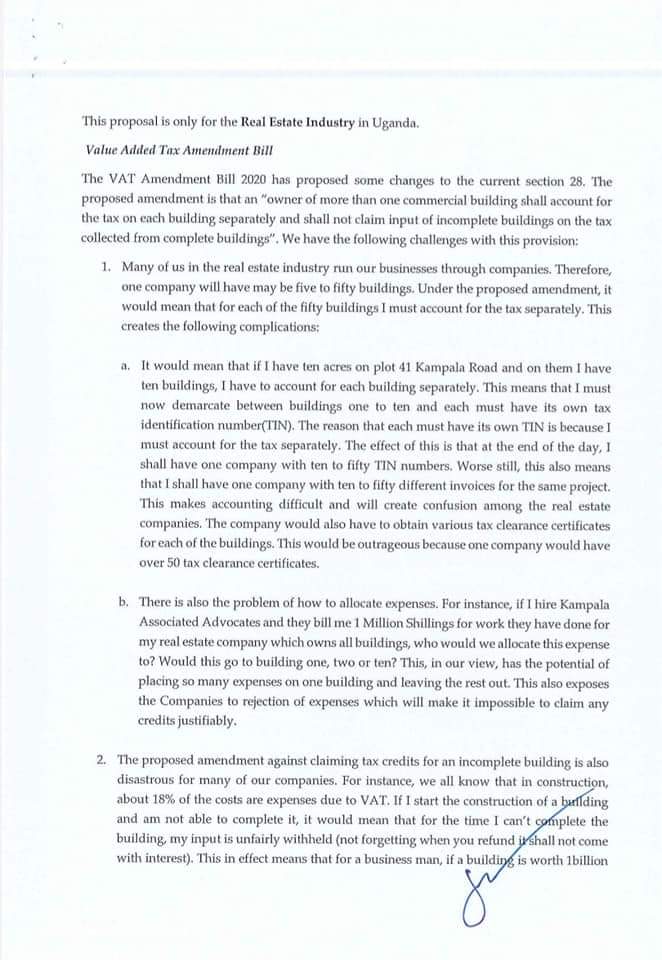

One of the bills which Meera Investments is contesting is the VAT Amendment Bill 2020, which has proposed some changes to the current section 28. The proposed amendment is that an “owner of more than one commercial building shall account for the tax on each building separately and shall not claim input of incomplete buildings on the tax collected from complete buildings.”

However, Meera Investments Ltd said many people in the real estate run their businesses through companies and “therefore, one company will have maybe five to fifty. Under the proposed amendment, it would mean that for each of the fifty buildings I must account for the tax separately.”

“It would mean that if I have ten acres on Plot 41 Kampala Road and on them I have ten buildings, I have to account for each building separately. This means that I must now demarcate between buildings one to ten and each must have its own tax identification number (TIN). The reason that each must have its own tax identification number (TIN) is that I must account for the tax separately. The effect of this is that at the end of the day, I shall have one company with ten to fifty TIN numbers. Worse still, this also means that I shall have one Company with ten to fifty different invoices for the same project. This makes accounting difficult and will create confusion among real estate companies. The company would also have to obtain various tax clearance certificates for each of the buildings. This would be outrageous because one company would have over 50 tax clearance certificates,” the petition states.

Part Of Meera Investments Petition reads in part

Meera Investments added that the proposed amendment against claiming tax credits for an incomplete building is also disastrous for many of our companies.

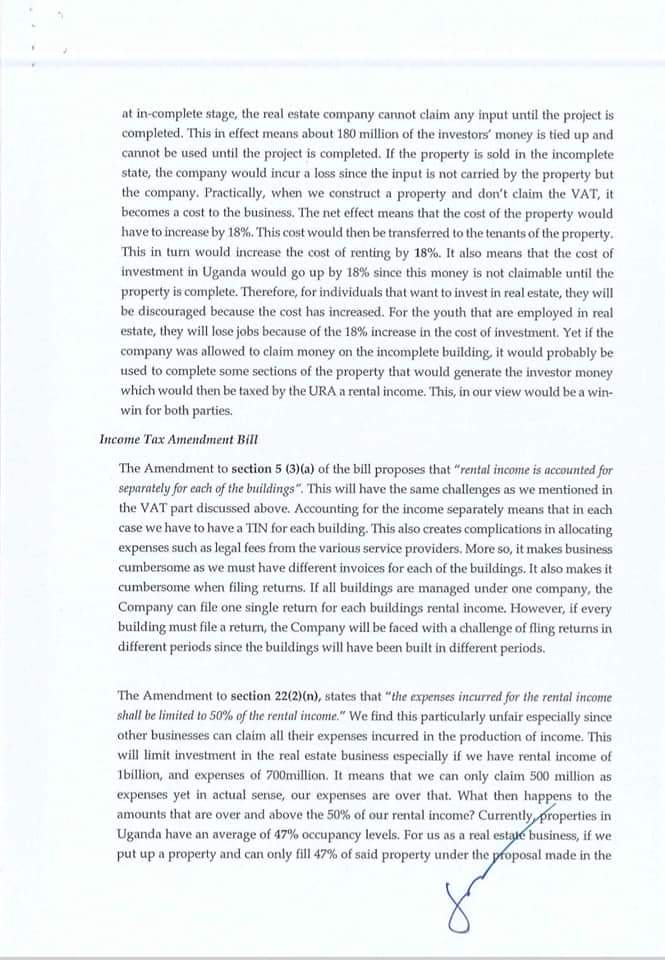

“For instance, we all know that in construction, about 98% of the costs are expenses due to VAT. If I start the construction of a building and am not able to complete it, it would mean that for the time I can’t complete the building, my input is unfairly withheld (not forgetting when you refund it shall not come with interest). This in effect means that for a businessman, if a building is worth 1billion at incomplete stage, the real estate company cannot claim any input until the project is completed,” the company states.

The company states that this in effect means about 180 million of the investors’ money is tied up and cannot be used until the project is completed. If the property is sold in the incomplete state, the company would incur a loss since the input is not carried by the property, but the company.

“Practically, when constructing a property and don’t claim the VAT, it becomes a cost to the business. The net effect means that the cost of the property would have to increase by 18%. The cost would then be transferred to the tenants of the property. This would in turn increase the cost of renting by 18%. It also means that the cost of Investment in Uganda would go up by 18% since the money is not claimable until the property is complete,” the company states.

Part Of Meera Investments Petition reads in part

Meera Investments Ltd is also opposed to the clauses in the Income Tax Amendment Bill, particularly section 5(3) (a) of the Bill which proposes that ‘rental income is accounted for separately for each of the buildings.’

“This will have the same challenges as we mentioned in the VAT part discussed above. Accounting for the income separately means that in each case we have to have a TIN for each building. This also creates complications in allocating expenses such as legal fees from the various service providers,” the company states.

“More so, it makes it cumbersome as we must have different invoices for each of the buildings. It also makes it cumbersome when filing returns. If all buildings are managed under one company, the company can file one single return for each building’s rental income. However, if every building must file a return, the Company will be faced with a challenge of filing return in different periods since the buildings will have been built in different periods,” the company adds.

Meera Investments Ltd is also opposed to Amendment to section 22 (2) (n), which states that “the expenses incurred for the rental income shall be limited to 50% of the rental income.”

“We find this particularly unfair especially since other businesses can claim all their expenses incurred in the production of income. This will limit investment in the real estate business especially if we have rental income of 1 billion, and expenses of 700 million. It means that we can only claim 500m as expenses yet in actual sense, our expenses are over that,” the company states.

Part Of Meera Investments Petition reads in part

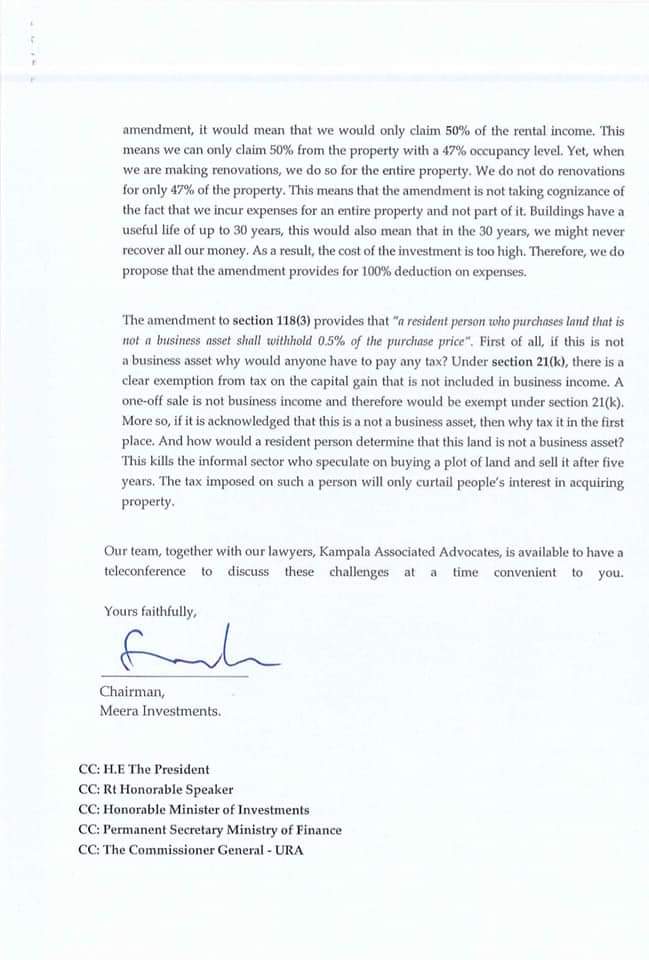

“What then happens to the amounts that are over and above 50% of our rental income? Currently, properties in Uganda have an average of 47% occupancy levels. For us as real estate business, if we put up a property and can only fill 47% of the said property under the proposal made in the amendment, it would mean that we would only claim 50% of the rental income. This means we can only claim 50% from the property with a 47% occupancy level.

Yet, when we are making renovations, we do so for the entire property. We do not to renovations for only 47% of the property. This means that the amendment is not taking cognizance of the fact that we incur expenses for an entire property and not part of it. Buildings have a useful life of up to 30 years, this would also mean that in the 30 years, we might never recover all our money. As a result, the cost of investment is too high. Therefore, we do propose that the amendment provides for 100% deduction on expenses.”

The company is also opposed to amendment to Section 118 (3) which provides that “a resident person who purchases land that is not a business asset shall withhold 0.5% of the purchase price.

“First of all, if this is not a business asset why would anyone have to pay any tax? Under section 21 (k), there is a clear exemption from tax on the capital gain that is not included in business income,” the company states.

“A one-off sale is not business income and therefore would be exempt under section 21 (k). More so, if it is acknowledged that this is not a business asset, then why tax it in the first place. And how would a resident person determine that this land is not a business asset? This kills the informal sector who speculate on buying a plot of land and sell it after five years. The tax imposed on such a person will only curtail people’s interest in acquiring property,” the company adds.

“Our team, together with our lawyers, Kampala Associated Advocates, is available to have a teleconference to discuss these challenges at a time convenient to you.”